16th Market Economy Colloquium: An Analysis of Factors Hindering SME Growth

-

Writer

Market Economy Colloquium

-

16th Market Economy Colloquium

Date and Time: June 19, 2026, 11:00 a.m.

Venue: Pureun Hall

Topic: An Analysis of the Factors Behind SMEs’ Refusal to Grow

Presenter: Philip Chung, Researcher, Center for Free Enterprise (CFE)

Discussants: Giman Kim, Secretary General, Good Regulation Citizens Forum; Jaewook Ahn, Emeritus Professor, Kyung Hee University; Sung-no Choi, President, Center for Free Enterprise (CFE); Yunseok Jung, Professor, Myongji College; Gwang yong Go, Policy Director, Center for Free Enterprise (CFE); and 6 others

An Analysis of the Factors Behind SMEs’ Refusal to Grow

Philip Chung, Researcher, Center for Free Enterprise (CFE)

1. Raising the Issue

Since the 1997 foreign exchange crisis, South Korea’s SME policy has consistently maintained a framework of fostering firms through support and protection. Yet despite the continued expansion of support, the outcome has been paradoxical. The productivity and wage gaps between large firms and SMEs have widened to among the largest in the OECD, while the layer of mid-sized firms that should form the backbone of the economy remains shallow.

This stagnation cannot be explained solely by the traditional diagnosis that “support is insufficient.” Rather, it raises a more fundamental question: is the support system itself distorting firms’ incentives to grow? This report finds the answer in the Peter Pan Syndrome. In other words, it refers to a phenomenon in which firms deliberately avoid growth even though they are capable of growing, because of incentive distortions created by the system. The core proposition is that this is not the result of a lack of entrepreneurship, but rather the outcome of rational choices made under the given institutional framework.

2. The Concept of the Peter Pan Syndrome and Its Economic Significance

The Peter Pan Syndrome originally refers in child psychology to a mindset in which a child refuses to become an adult. When applied to firms, it is limited to cases where incentives exist to avoid growth. It is distinct from structural constraints that prevent firms from growing, such as capital shortages, insufficient technological capabilities, or limited market demand. Instead, it refers to situations in which non-market institutions such as regulations or subsidies distort growth incentives, leading firms to choose not to grow. This distinction is important from a policy perspective. Growth constraints caused by market failure may justify intervention through support, but growth avoidance caused by institutional failure instead calls for reducing and redesigning intervention.

In a market economy, firm growth is a key mechanism for improving the efficiency of resource allocation, realizing economies of scale, and promoting innovation and productivity gains. As Schumpeter pointed out, the process by which highly productive firms grow while less productive firms exit raises overall economic productivity. However, Korea’s SME support system operates in a way that weakens this selection function. Low-productivity firms remain in the market by relying on subsidies, while even highly productive firms avoid mid-sized firm status, thereby reducing the dynamic efficiency of the entire business ecosystem.

Its macroeconomic implications are threefold. First, it distorts resource allocation. When firms with growth potential voluntarily limit their scale, capital remains stuck in less productive uses and labor becomes fixed in workplaces that fail to realize economies of scale. Second, it entrenches the dual structure. The divide between a small number of large firms and a large number of small SMEs becomes institutionally fixed. As of 2024, the number of mid-sized firms stood at 6,474, appearing to increase on the surface, but within that total, hundreds of firms return to SME status each year and even more consider doing so. This stagnation cannot be captured through static indicators alone. Third, it weakens innovation incentives. When subsidies and tax benefits function as rewards for “staying small,” firms choose maintaining the status quo over innovating through expansion, thereby weakening the mechanism of progress through creative destruction and ultimately lowering the long-term potential growth rate.

Source: Qiao & Fei (2022); Chang et al. (2021); Peek & Rosengren (2005)

3. Mechanism of Growth Avoidance (1): Subsidies Unrelated to Productivity

The first mechanism that creates incentives to avoid growth is the structure of subsidy provision unrelated to productivity. According to the Bank of Korea’s “Current Status of SMEs in Korea and Measures to Improve the Support System,” a regressive structure has emerged in which firms with lower profitability, growth, and productivity receive more direct and indirect government support. In other words, the share of support has a negative correlation with productivity, profitability, and growth.

This distortion operates through two channels. One is the prevention of market exit by marginal firms. Subsidies provided regardless of productivity function as a soft budget constraint for marginal firms, making them less sensitive to debt levels, asset soundness, and interest rate changes, and causing them to lose the motivation to generate profits independently. In addition, subsidies serve as a positive signal for external financing, encouraging banks to continue forbearance lending that bypasses normal credit evaluation, thereby creating a vicious cycle of “moral hazard → government subsidies → bank lending → moral hazard” (Peek and Rosengren, 2005; Qiao and Fei, 2022). The other is a decline in the marginal benefit of growth efforts. As high-performing firms are excluded from support, the reward for trying to grow is structurally reduced.

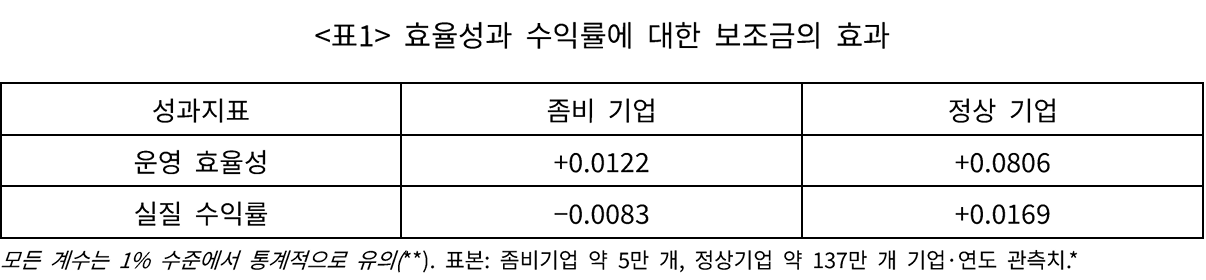

These concerns are supported empirically. The OECD’s The Market Implications of Industrial Subsidies shows that subsidy provision itself contributes very little to productivity improvement, suggesting that subsidies to low-productivity firms do not create a virtuous cycle of “support → productivity improvement → self-sustaining growth.” Qiao and Fei (2022), using data on Chinese industrial firms, are more specific. In an analysis of approximately 1.42 million firm-year observations from 1998 to 2013, government subsidies were found to improve both operating efficiency and real returns for ordinary firms, whereas for zombie firms, even where operating efficiency improved somewhat, real returns actually declined significantly—revealing an asymmetric effect. In other words, subsidies may enable the short-term survival of marginal firms, but they do not lead to a fundamental recovery in competitiveness; instead, they entrench firms in a state of being “alive but unable to recover.” The authors identified moral hazard as the key mechanism: while subsidies mitigated moral hazard in ordinary firms, they actually increased moral hazard in zombie firms, and the negative effect was stronger the smaller the zombie firm and the lower its market share.

Source: Qiao and Fei (2022)

The same structure is unfolding in Korea. According to a 2022 analysis of externally audited corporations by the Future Strategy Research Institute of KDB Industrial Bank, the number of marginal firms with an interest coverage ratio below 1 for three consecutive years rose about 3.3 times, from 1,353 in 2011 to 4,478 in 2021. Over the same period, the share of marginal firms among those analyzed also increased from 10.2% to 18.3%. In particular, the number of small marginal firms rose 3.5 times, from 1,225 to 4,288, driving the quantitative expansion. More worrying is the chronic nature of the problem. During the analysis period, firms classified as marginal at least twice accounted for 23.1% of the total, up 9.8 percentage points from 13.3% in 2016. The number of firms reporting operating losses for three consecutive years also more than quadrupled, from 615 (2011) to 2,519 (2021). The median debt dependence ratio of marginal firms was 48.3%, far above that of non-marginal firms (29.7%), while the debt repayment period relative to EBITDA was about 9 years, three times that of non-marginal firms (about 3 years). This means that, on the basis of their own operating cash-generating capacity, repayment is virtually impossible and survival depends on external funds. It is direct evidence that the mechanism of “preventing market exit through a soft budget constraint” is actually at work.

4. Mechanism of Growth Avoidance (2): Stepwise Regulation and the Support Cliff

The second mechanism is the stepwise increase in regulation and interruption of support based on asset size. In Korea, corporate regulation increases in stages as asset size grows (SME → mid-sized firm → quasi-large firm → large firm). According to the Korea Enterprises Federation’s “2023 Survey on the Status of Discriminatory Regulations Against Large Companies,” the marginal increase in regulation is greatest when an SME grows into a mid-sized firm, with newly designated mid-sized firms becoming subject to 126 new regulations at once.

At the same time that regulation increases, support is cut off sharply. According to Bank of Korea research, about 40% of firms in the range just below the threshold for mid-sized firms (0.9–1.0 times the revenue threshold) receive government support, but the benefit rate falls sharply the moment they exceed the threshold and are recognized as mid-sized firms. This creates a so-called “cliff” structure in which costs rise while benefits are cut off. As a result, the increase in costs and loss of benefits imposed merely for slightly exceeding the threshold can become so large that there emerges a range in which the marginal benefit of growth is smaller than its marginal cost. In effect, firms face a strong incentive to intentionally suppress growth below the threshold.

Firm Size | Asset Size | Number of New Regulations

Firm Size

Asset Size

Number of New Regulations

SMEs

Total assets of KRW 50 billion or more

4

Total assets of KRW 100 billion or more

15

Total assets of KRW 300 billion or more

38

Mid-sized firms

Total assets of KRW 500 billion or more

126

Total assets of KRW 1 trillion or more

2

Total assets of KRW 2 trillion or more

24

Large firms

Business groups subject to disclosure (total assets of KRW 5 trillion or more)

65

Business groups subject to cross-shareholding restrictions (total assets of KRW 10 trillion or more)

68

Source: Korea Enterprises Federation, “2023 Survey on the Status of Discriminatory Regulations Against Large Companies”

5. Empirical Consequence: Mid-sized Firms Returning to SME Status

The consequences of these two mechanisms can be directly observed in the Ministry of Trade, Industry and Energy’s “2023 Basic Statistics on Mid-sized Firms.” As of the 2023 fiscal year-end, there were 5,868 mid-sized firms. Of the 744 firms excluded from mid-sized firm status that year, as many as 574 (77.2%) did not grow into large firms but instead returned to SME status. The fact that more firms reverted to SME status than the combined total of temporary suspension/closure (65 firms) and entry into the large-firm category (105 firms) suggests that mid-sized firm status itself is not attractive to many firms.

Source: Ministry of Trade, Industry and Energy, “Results of the 2023 Basic Statistics on Mid-sized Firms”

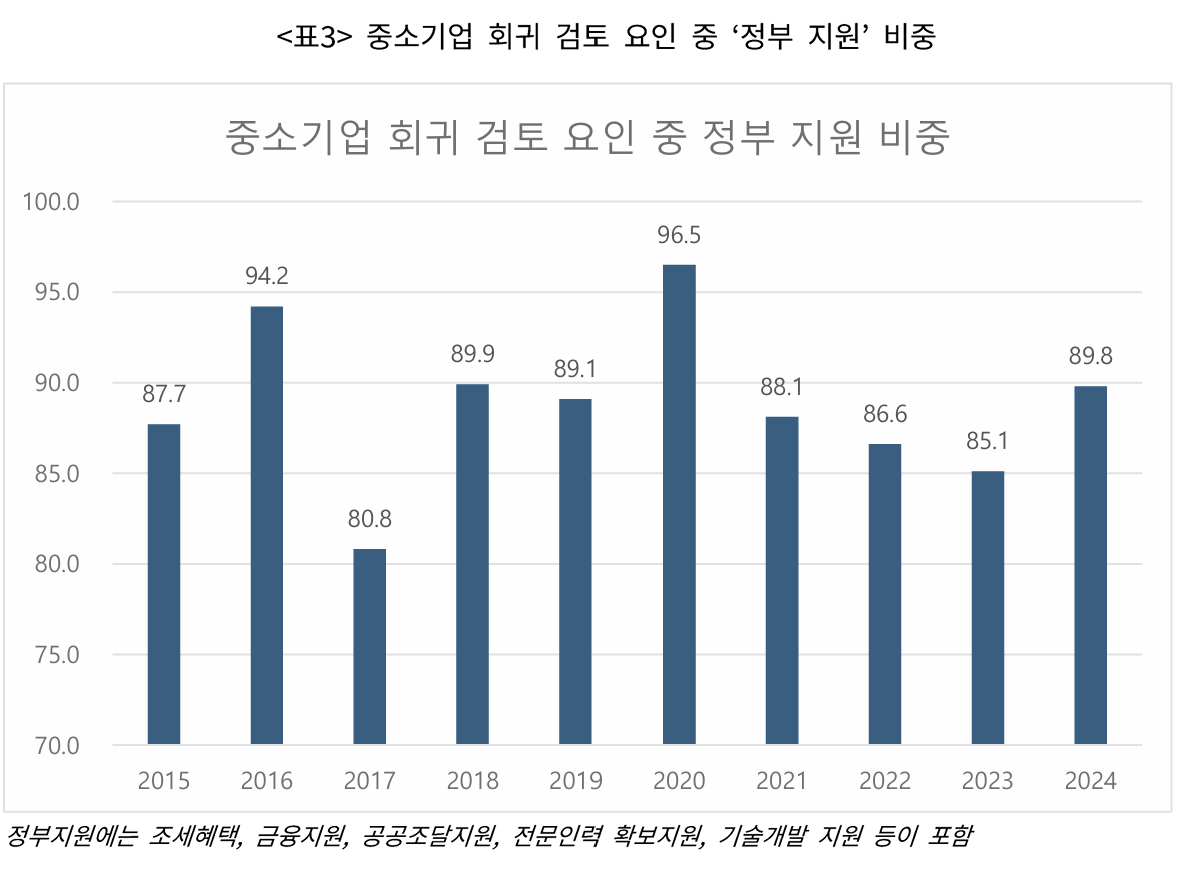

The share of firms actively considering a return is also increasing over time. The proportion of mid-sized firms considering a return to SME status rose from 5.3% in 2022 to 6.1% in 2023. The top reason for considering a return was the reduction of tax support (60.8%), followed by SME-suitable industries (14.9%), reduction of financial support (14.2%), and sales channel restrictions such as the public procurement market (6.3%). The fact that more than 75% of the reasons for considering a return are directly related to the “loss of support” shows that the cost-benefit structure associated with becoming a mid-sized firm is designed so unfavorably that it can cause firms to reverse their growth decisions after the fact. In the same survey, the areas in which mid-sized firms most wanted expanded support were also taxation (36.6%) and finance (34.3%), which together accounted for 70% of responses. This means that the current system effectively cuts off tax and financial support at the mid-sized firm stage in cliff-like fashion, to the point that even firms that have already grown do not have the capacity to absorb the discontinuity.

In short, Korea’s corporate ecosystem is trapped in a dual stagnation in which firms neither grow upward nor are reorganized downward. At the lower end of the market, marginal firms are expanding in number and becoming chronic, paralyzing the natural process of market淘汰. In the middle tier, hundreds of firms voluntarily return to SME status every year. The Peter Pan Syndrome is not a hypothetical concern but a measurable phenomenon that is renewed every year in Korean corporate statistics.

6. Policy Recommendations

Accordingly, policy should not be directed simply toward either expanding or reducing support, but toward redesigning the linkage structure between support and regulation itself. This report offers five recommendations.

1. Shift support criteria from size to performance.

Change support criteria from firm size to performance indicators such as productivity, innovation, and growth potential. This would allow the natural exit of marginal firms while concentrating support on firms with both the willingness and the capacity to grow.

2. Introduce a gradual graduation system.

Instead of a cliff structure in which all support is cut off and regulations are imposed at once upon becoming a mid-sized firm, support should be reduced gradually and regulations applied step by step over a set period (e.g., 5–7 years). There are international benchmarks for such buffer-zone systems in the EU and Japan, among others, and given that the top reason for considering a return is the reduction of tax support (60.8%), a phased easing on the tax side is most urgent.

3. Manage the total volume of regulations.

For the 126 regulations automatically applied based on asset size, individual regulatory impact analyses (RIA) should be conducted so that only those whose practical necessity is verified are retained.

4. Improve the design of tax incentives.

The criteria for tax benefits should be linked not to “maintaining SME status” but directly to growth-oriented corporate behavior such as R&D investment, job creation, and innovation activities. The aim is to select beneficiaries based not on firm size but on firm behavior.

5. Improve exit pathways for marginal firms.

For the market’s selection function to work properly, orderly exit for marginal firms must be possible. This requires safety nets that reduce the social costs of exit—such as simplified bankruptcy and rehabilitation procedures, support for restarting businesses, and worker retraining—so that market dynamism can be restored instead of firms merely surviving on subsidies.

7. Conclusion

The refusal of Korean SMEs to grow—that is, the Peter Pan Syndrome—is not a phenomenon arising from moral hazard on the part of firms or a lack of entrepreneurship, but the result of rational choices created by the system. In a structure where subsidies and tax benefits are concentrated on low-productivity firms, and where the rewards for growth are offset by increased regulatory burdens and the loss of benefits, it is economically rational for firms to avoid growth. The empirical evidence reviewed in this report—the KDB analysis of marginal firms, the Ministry of Trade, Industry and Energy’s statistics on mid-sized firms returning to SME status, and Qiao and Fei’s study of zombie firms—consistently supports this conclusion.

Accordingly, the solution lies not in moral persuasion directed at firms, but in building an institutional environment in which growth becomes the rational choice. This cannot be achieved by either reducing support or strengthening regulation alone. It requires a fundamental approach that redesigns the linkage structure between support and regulation itself. If the essence of a market economy lies in the dynamic process through which resources move to their most productive uses, then the current SME support system is operating not to complement that self-adjusting function but rather to hinder it. The Peter Pan Syndrome is the clearest evidence of this problem, and it suggests that the time has come for a fundamental reexamination of SME policy.

References

• National Tax Service and Ministry of SMEs and Startups, 2025 SME Tax and Tax Administration Support System

• Chanu Park (2022), “The Current Status and Implications of Marginal Firms,” KDB Monthly Bulletin of Industrial Economy No. 800, Future Strategy Research Institute, KDB Industrial Bank

• Ministry of Trade, Industry and Energy, “Results of the 2023 Basic Statistics on Mid-sized Firms,” December 2024

• Korea Enterprises Federation, “2023 Survey on the Status of Discriminatory Regulations Against Large Companies”

• Bank of Korea, “Current Status of SMEs in Korea and Measures to Improve the Support System”

• Bank of Korea, Financial Stability Report (June 2015, December 2015, June 2021)

• OECD, The Market Implications of Industrial Subsidies

• Caballero, R. J., Hoshi, T., and Kashyap, A. K. (2008). Zombie lending and depressed restructuring in Japan. American Economic Review, 98(5), 1943–1977.

• Chang, Q., Zhou, Y., Liu, G., Wang, D., and Zhang, X. (2021). How does government intervention affect the formation of zombie firms? Economic Modelling, 94, 768–779.

• Peek, J., and Rosengren, E. S. (2005). Unnatural selection: Perverse incentives and the misallocation of credit in Japan. American Economic Review, 95(4), 1144–1166.

• Qiao, L., and Fei, J. (2022). Government subsidies, enterprise operating efficiency, and "stiff but deathless" zombie firms. Economic Modelling, 107, 105728.

• Tan, Y., Tan, Z., Huang, Y., and Woo, W. T. (2017). The crowding-out effect of zombie firms: Evidence from China’s industrial firms. Economic Research Journal, (5), 175–188.

• Zmijewski, M. E. (1984). Methodological issues related to the estimation of financial distress prediction models. Journal

Original title: 제16회: 중소기업 성장 거부 요인 분석

Author: Center for Free Enterprise (CFE)

Date: 2026-06-19

Source: https://www.cfe.org/bbs/bbsDetail.php?cid=collo&pn=1&idx=29182