Key Issues and Critical Analysis of the Proposed Sugar Levy (Sugar Tax)

-

Writer

CFE

-

1. Overview and Background of Introducing a Sugar Levy

1. Overview and Background of Introducing a Sugar Levy

President Lee Jae-myung proposed, via social media (SNS), the idea of imposing a health promotion levy on sugar-added beverages, commonly referred to as a sugar tax. The presidential office mentioned a plan to “discourage consumption through a sugar levy, as with tobacco taxes, and reinvest the revenue into strengthening regional and public healthcare.” According to media reports, it also cited a poll showing that about 80% of the public supports the measure. International organizations such as the WHO have recommended the introduction of sugar taxes since 2016, and roughly 120 countries, including the UK, France, and Mexico, are implementing similar policies. In Korea as well, the idea has already been discussed several times in political and academic circles since the 2020s, and in 2021, a bill was introduced under the lead sponsorship of Rep. Kang Byeong-won to impose a National Health Promotion Charge on sugar-sweetened beverages, though it was later scrapped due to industry opposition and other factors.

In Korea, excessive sugar consumption has been identified as a cause of obesity and diabetes, while social costs are rising—for example, estimated at KRW 16 trillion annually—so there is some positive discussion around adopting such a policy. However, past policy experiments involving various health taxes and a range of studies have also revealed significant problems. Accordingly, this issue report critically examines, from multiple perspectives, the appropriateness of introducing a sugar levy (so-called sugar tax) and offers policy recommendations.

2. The Quasi-Tax Nature and Problems of a Sugar Levy

The government is emphasizing that it intends to pursue this proposal not as a tax but in the form of a “charge.” According to media reports, while a sugar tax is closer to a general excise tax, a sugar levy is described as “a quasi-tax charge used only for health promotion programs.” In fact, the Ministry of Economy and Finance and the Ministry of Health and Welfare have stated that, unlike general tax revenue, levy revenue would be used solely for health promotion purposes, such as support for healthy lifestyles, nutrition management, and the expansion of public healthcare.

However, even if it is labeled a “levy,” in substance it is no different from a consumption tax. A levy differs formally from a general tax in that it is imposed on those who cause a specific public-interest problem or benefit from it, for a designated public purpose. For this reason, the government explains that a sugar tax is a tax, while a sugar levy is a quasi-tax charge. Economically, however, it amounts to a higher consumption tax and therefore ultimately increases the burden on the public. Although levy revenue is allocated to a specific fund rather than the general account, ordinary citizens can hardly perceive any practical difference in spending structure or use of funds. Because of these characteristics, levies are often called “shadow taxes” or “quasi-taxes.”

Ultimately, regardless of its name, a sugar levy is a policy tool that increases the public’s burden and has the same economic effect as a tax. Ignoring this substantive reality in policy discussions while stressing only formal distinctions may undermine the credibility of the policy.

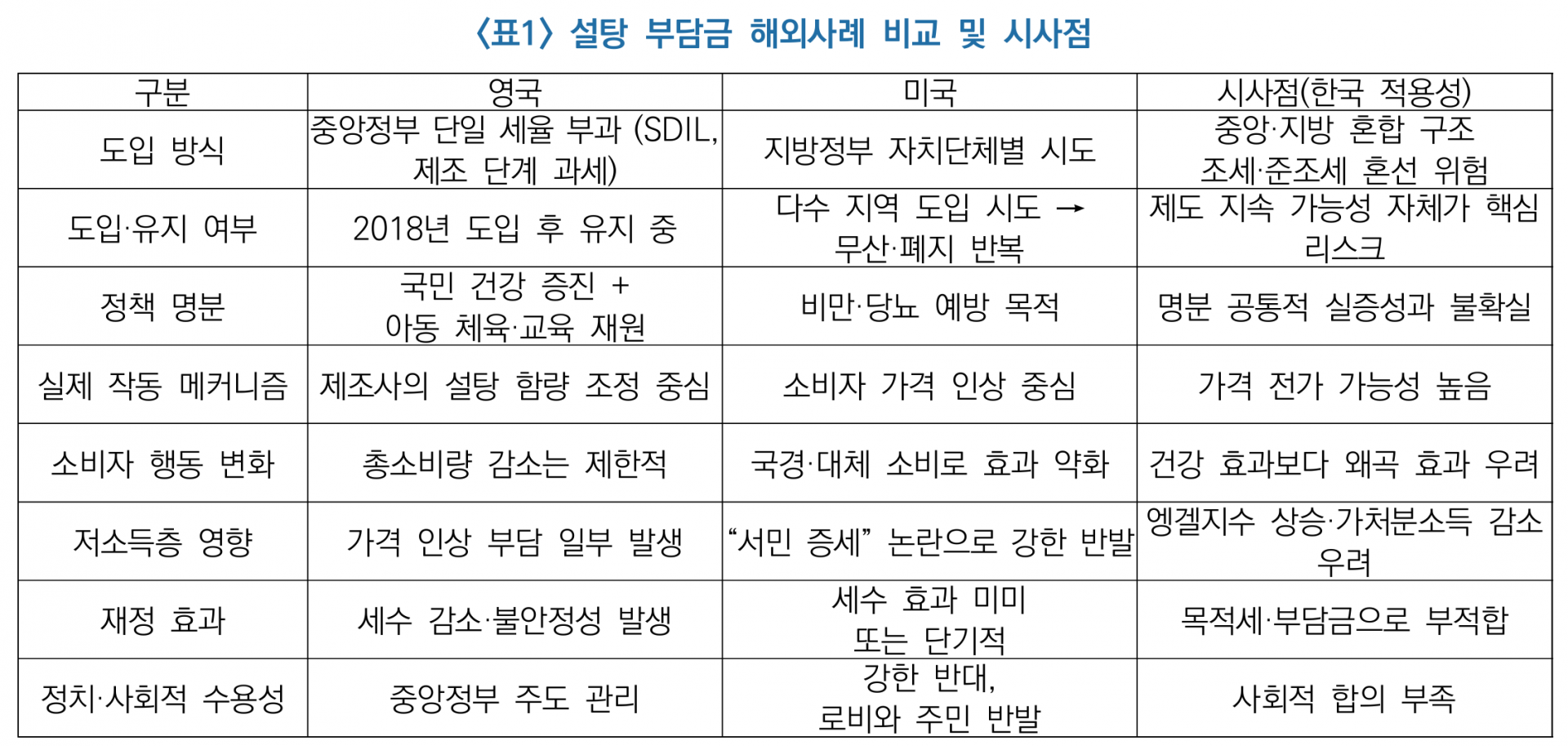

3. Overseas Cases and Implications for Korea

◩ Overseas Cases and the Unsuitability of Direct Application to Korea

The UK introduced the Soft Drinks Industry Levy in 2018, applying progressive tax rates based on sugar content. After its introduction, the average sugar content of covered beverages fell by about 47%, and 65% of beverage companies changed their formulations to reduce sugar content below taxable thresholds. Mexico imposed a 10% tax on soft drinks in 2014, and in the first year consumption fell by about 7%, with a particularly sharp decline among low-income households. These cases show both reduced sugar intake and expanded public revenue, but their economic and consumption structures differ from Korea’s. For example, Korea’s carbonated beverage market is relatively small, and there is an abundance of substitutes such as coffee drinks and snack foods.

France introduced a sugar tax in 2012, but its effect was limited because the rate was low at EUR 0.076/L. At the time of introduction, the government emphasized health as its rationale, but it soon shifted to stressing fiscal balance and using it as a source of health insurance funding, drawing criticism. In the 2018 revision, the tax system was strengthened to impose differentiated rates according to sugar content.

More than 100 countries have introduced sugar taxes or similar systems. The UK adopted a system imposing differentiated charges according to the sugar content of sugar-sweetened beverages, thereby inducing companies to reformulate products. France likewise taxes beverages in proportion to their sugar content and uses the revenue for social security financing.

There are several structural differences, however, that make it inappropriate to apply these cases directly to Korea. First, Korea’s sugar consumption structure is not centered on carbonated drinks but is spread across coffee beverages, confectionery and baked goods, and processed foods. Korea’s per capita sugar consumption is relatively low—for example, according to OECD projections, HFCS consumption in Japan and Korea is around 5 kg—and major sugar sources are also dispersed across juice, desserts, and processed foods. Even if a policy was effective in advanced economies, its effectiveness has not been verified in light of Korea’s consumption patterns and market structure. If levies are imposed only on specific items, substitute consumption is likely to occur, limiting any real health improvement.

Second, Korea is already in a high-inflation environment, with rising food and dining-out costs placing a heavy burden on households. In addition, under Korea-specific price conditions—including exchange rates and rising distribution and manufacturing costs—a higher consumption tax could add inflationary pressure. In this situation, any additional factor driving up prices could significantly reduce policy acceptance.

In some countries, a sugar tax initially reduced consumption, but over time its effect weakened, and side effects such as cross-border or interregional “shopping trips” increased. This shows the limits of relying on price signals alone to fundamentally change eating habits.

◩ Failed Sugar Tax Attempts in the United States and Their Implications

The United States has seen some of the fiercest legal and political battles between public health authorities and the beverage industry over sugar taxes or soda taxes. Before Berkeley, California became the first U.S. locality to introduce a sugar tax in 2014, about 30 local governments had attempted similar systems, but most failed. Even after adoption, many regions faced strong resistance or later repealed the policy.

A representative failed case is New York City. During the tenure of Mayor Michael Bloomberg, the city attempted to restrict the sale of large-sized sugary drinks and impose additional charges, but amid large-scale lobbying by the beverage industry and expanding criticism that the policy was regressive toward low-income groups, it collapsed at the court review stage. Another case is Cook County, Chicago, Illinois. The county introduced a sugar tax of 1 cent per ounce in 2017, but amid consumer backlash and organized opposition campaigns by the retail and distribution industries, the system was repealed after just 5 months. A sharp rise in purchases from neighboring areas to avoid the tax, which weakened local commercial districts, was also cited as a major reason for repeal.

The industry also used a strategy of enacting state-level “preemption laws.” In several states, including California, Michigan, and Washington, laws were passed preventing local governments from independently imposing sugar taxes, effectively halting such efforts in cities including Santa Cruz.

The U.S. case shows that a sugar tax can quickly expand beyond a simple public health issue into broader problems involving local economies, consumer burdens, and tax fairness. In particular, when only beverages are taxed, substitution toward other high-sugar foods and “shopping trip” consumption shifting to neighboring areas became key factors weakening policy effectiveness.

These experiences suggest that a sugar levy in Korea could similarly trigger political and social conflict. The U.S. experience, in which policy sustainability was not secured even at the city level despite comparable consumption structures, should serve as an important warning sign for Korea, where a nationwide policy is being discussed at the central-government level.

4. A Multidimensional Analysis of the Problems with a Sugar Levy

◩ Inflation, Burden-Shifting to Low-Income Households, and Reduced Disposable Income

If a sugar levy is introduced, manufacturers are highly likely to pass the cost on through higher product prices. Media outlets including Kyunghyang Shinmun have pointed out that “if the rise in costs is passed directly onto consumer prices, prices will rise in a chain reaction not only for carbonated drinks but also for similar product categories.” In the end, consumers will feel either a “sugar tax” or a “sugar levy” as a bill they have to pay.

At that point, the burden on lower-income groups will be especially severe. Because a sugar tax imposes the same rate regardless of income, it creates regressive tax burdens. A report by the National Assembly Research Service also stated that “a sugar tax places a relatively heavier burden on low-income groups whose ability to switch to substitutes is limited.” Actual statistics also show that the share of food spending among low-income households in Korea—the Engel coefficient—is among the highest of all income groups. According to Kyunghyang Shinmun, if only grocery spending is counted, excluding self-employment and dining out, the lowest-income group spent as much as 21.6% of expenditures on food, and the ratio is even higher when dining-out costs are included. For such households, higher food prices deal a major blow to real disposable income.

The UK also experienced a pass-through problem. Some beverage prices rose, lower-income groups were more price-sensitive and therefore bore a more concentrated real burden, and even the cost of switching to sugar-free products ultimately fell on consumers. This shows that a sugar tax can ultimately function as a regressive consumption tax that restricts freedom of consumer choice.

As a result, higher prices for sugar-containing beverages and similar products are likely to put pressure on the cost of living of low-income households, raising the Engel coefficient and reducing real disposable income.

◩ Reexamining the UK Sugar Tax and Its Lessons

(1) Product Reformulation, Not Reduced Consumption

The UK’s Soft Drinks Industry Levy (2018) is often presented as a successful case of obesity prevention. But the actual outcome can be summarized as follows. First, the change in consumer behavior—namely a decline in the consumption of sugar-added products—was limited. Total carbonated beverage consumption itself did not decline dramatically, and consumers shifted instead to low-sugar products, smaller package sizes, or alternative drinks.

Second, the substance of the policy effect was not “suppressed consumption” but “manufacturer recipe changes.” Large beverage companies reduced sugar content below the threshold to avoid the tax, so the tax functioned less as a behavior-correction tool than as a regulatory compliance cost. In other words, it is difficult to empirically demonstrate a direct health improvement effect, while the market restructuring effect caused by regulation was relatively more apparent.

(2) Empirical Limits Regarding Health Outcomes

Studies by UK health authorities and academia have repeatedly pointed to the following limitations. First, there is insufficient evidence that the sugar tax brought about a meaningful decline in obesity rates or diabetes prevalence. Declines in obesity among children and adolescents were difficult to distinguish from long-term trend changes. Second, because key factors such as lack of exercise, overall diet, and income and housing conditions remained separate influences, the causal effect of the policy was unclear. It was difficult to isolate the independent effect of the sugar tax from the effects of school meal regulations and education policies implemented at the same time. As a result, the simple causal claim that the sugar tax’s fundamental purpose was “improved health” was not proven.

◩ Fiscal Paradox and the Instability of Earmarked Taxes: It May Fail to Catch Either “Health Promotion” or “Revenue Raising”

The government says that sugar levy revenue will be used only for health promotion projects, but actual cases show that a healthcare rationale can easily deteriorate into a mere revenue-raising tool. As in France, a tax initially justified on health grounds later shifted into a means of “balancing the national budget,” weakening its original health-promotion function.

When introducing the sugar tax, the UK government cited “improving children’s health and securing funding for sports and education” as its rationale. But the actual outcome was, first, unstable tax revenue. Revenue rose at first, but as manufacturers reduced sugar content, actual medium-term revenue fell significantly below projections. It therefore lacked sustainability as a funding source for earmarked programs.

Second, it was effectively absorbed into general fiscal spending. In some years, the revenue was incorporated into the general budget regardless of the designated purpose, creating an internal conflict between the policy objective (improving health) and the fiscal objective (raising revenue). This shows that a sugar tax is a system with a high likelihood of failure even as an earmarked tax.

In this way, earmarked taxes for specific purposes, such as health taxes, may be treated as stable revenue sources, causing rigidity in budget allocation and reducing fiscal transparency. Even if nominally a “health fund,” once the revenue scale grows, the government as a whole tends to become more dependent on it. Consumers ultimately bear only higher prices, while from the government’s perspective the likelihood of turning it into a permanent revenue source rises, producing policy inefficiency.

5. Conclusion and Policy Implications

A sugar levy is formally a levy, but in substance it is a new indirect tax. It is difficult to justify its introduction on the basis of overseas cases, because Korea’s consumption structure and economic conditions differ, while side effects such as inflation and heavier burdens on low-income groups are significant. Above all, an earmarked-tax approach that seeks to secure revenue under the banner of health promotion may distort fiscal policy.

What is needed now is not another quasi-tax, but the restoration of fiscal soundness through stronger fiscal rules and spending restructuring. The sugar levy debate must not become a means of obscuring these fundamental tasks. The current government is already facing calls for the introduction of fiscal rules amid conditions such as national debt surpassing KRW 1 quadrillion, and in the 2026 budget proposal it carried out restructuring by cutting approximately KRW 27 trillion in spending across 1,300 programs.

First, fiscal resources should be secured by restoring fiscal rules and strengthening expenditure restructuring and debt management. Targets for national debt and fiscal deficits should be codified into law so that tax revenue and expenditure can be managed strictly, while budgets should be made more efficient by focusing on high-return, high-cost programs. Unnecessary levies need to be reduced. If necessary, welfare and health sectors should also be included to cut waste and overlapping budgets, and spending should be shifted toward priority growth investments such as science and technology and social overhead capital. Second, instead of introducing new tax bases or levy schemes, more fundamental alternatives for health promotion should be sought. Rather than a sugar tax, non-tax policies should be prioritized, such as expanding health education and nutrition management programs by income group and encouraging voluntary reformulation.

The introduction of a sugar levy may help secure short-term revenue, but in the long run it is highly likely to increase household burdens and hinder economic vitality. Given its quasi-tax nature, the introduction of a sugar levy is difficult to justify as health policy, fiscal policy, or redistribution policy. Balanced policy judgment that takes account of Korea’s economic and social structure is needed, and if the goal is to raise revenue, the government should focus first on fundamental measures such as expenditure restructuring and debt management rather than tax increases.

◩ References

● Rep. Kang Byeong-won, “Partial Amendment to the National Health Promotion Act (Sugar-Sweetened Beverage Charge),” 2021.

● Korea Institute of Public Finance, Study on Taxation of Sugar-Sweetened Beverages, 2022.

● National Assembly Research Service, Review of Tax Policy for Obesity Prevention, 2021.

● Statistics Korea, Household Trends Survey, latest year.

● JoongAng Ilbo, “'Let’s Collect a Sugar Levy Like Tobacco Taxes’… The Sugar Tax Debate,” 2026.1.

● News Tomato, “Fact Check: Is It a Sugar Tax or a Sugar Levy?,” 2026.1.

● Maeil Business Newspaper, “Controversy After Lee’s Remarks on 'Reinvesting Sugar Levy Revenue in Regional Healthcare,’” 2026.1.

● World Health Organization (WHO), Fiscal policies for diet and the prevention of noncommunicable diseases, 2016.

● OECD, The Heavy Burden of Obesity: The Economics of Prevention, 2019.

● UK Government, Soft Drinks Industry Levy: Impact Assessment, 2018.

● Tax Foundation (US), Sugar-Sweetened Beverage Taxes, various years.

Wiki:

https://www.cfe.org/w/bbsDetail.php?&idx=22

Original title: 설탕 부담금(설탕세) 도입 논의의 쟁점과 비판적 분석

Author: Center for Free Enterprise (CFE)

Date: 2026-01-30

Source: https://www.cfe.org/bbs/bbsDetail.php?cid=issue&pn=1&idx=28582